In May, Pick n Pay revealed a major restructuring plan to bolster its financial position and improve its market share. A key component of this overhaul involves the separate listing of its cash cow Boxer discount chain on the JSE later this year, through which the group is aiming to raise between R6-billion and R8-billion.

To streamline operations, Pick n Pay is also converting about 45 of its traditional stores into franchise outlets, and plans to create smaller, more profitable Pick n Pay stores tailored to specific customer needs.

If the broader strategy to enhance product offerings, optimise store operations and strengthen customer relationships works, PnP hopes to be profitable once again by 2027.

While maintaining majority control over Boxer, PnP will now be fighting for market share against Shoprite, but it will be doing so on two fronts: against Shoprite and Usave on one side, and independent retailers such as Cash and Carry on the other, analysts say.

Although Boxer has a larger footprint than Usave, Shoprite is a juggernaut in townships, towns and rural areas.

In February 2024, Boxer SA’s footprint was 477 stores (including 31 BuildIt and 150 liquor stores), with 287 supermarkets. Usave’s SA footprint was 453 stores, bolstered by 628 Shoprite stores in SA (plus 464 Shoprite LiquorShop stores).

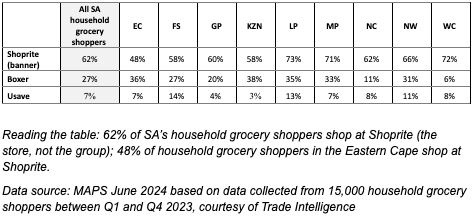

Senior analyst at Trade Intelligence Nicola Allen says the Shoprite brand has much greater penetration into the SA household shopper universe than Boxer, but Boxer far outstrips Usave.

“There are regional nuances, too – Usave outstrips Boxer in the Western Cape (although both are minnows and Shoprite is particularly strong) and Boxer is a credible challenger to Shoprite in the Eastern Cape, which is Shoprite’s weakest province.”

Boxer, founded in 1977, is an established chain that holds its own in certain areas against Shoprite, which has the advantage of having a stable of four brands (Shoprite, Usave, Checkers and Checkers Hyper). “It’s a strong brand in itself, and will continue to be so,” she says.

Achumile Mashalaba from NinetyOne says ShopRite is expanding and taking a low-frills approach, while Boxer faces difficulties in reaching its target due to stiff competition. “Boxer competes with both Usave and Shoprite stores. USave is more of an everyday type of shop, where people can go and get whatever they need, in small baskets, but when it’s payday or after the big grant payments, people tend to travel more to go to a Shoprite store, which is generally much bigger.”

From an SKU perspective (the stock-keeping unit used to identify finished goods that are sold to customers), Usaves generally have between 1,000 to 2,000 SKUs, while Boxer is a larger format, generally targeting 3,000 SKUs.

For post-payday shopping, Boxer is competing with a combination of both Shoprite and Usave.

“The beauty about the Usave model is, because it has a low number of SKUs, you can have a really small store of 200 square metres, or a store that’s closer to 1,000 square metres, because the offering is super no-frills.”

Shoprite launched Usave in 2001, while PnP acquired Boxer in 2002. With PnP targeting the middle and upper income groups, which pits it against Checkers and Woolworths at the top end of the market, Shoprite aims at the middle and lower segments and both Usave and Boxer target the bottom end of the market.

In February, Eighty20’s retail wrap, using both MAPS (a quarterly, nationally representative survey of 20,000 people) and BrandMapp (an annual online survey of 35,000 people in households with incomes more than R10,000 per month) found Shoprite and Checkers enjoyed 16% and 19% growth in customers respectively in 2023, with Pick n Pay and Woolworths in a “holding pattern”. Shoprite and Checkers have gained significant market share due to enhanced rewards programmes, rapid delivery services and a perceived price advantage, leading to a mass exodus of customers from competing retailers.

Boxer and Usave are both more affordable options, but they differ in terms of their store formats: Usave is a compact, convenient store, while Boxer is a larger format store.

“Boxer is (likely to) carry on doing what’s always done and they’re doing a fantastic job. The bigger problem for PnP is their positioning — they only have the PnP brand, while the Shoprite group has various brands at different segments.”

Mashalaba says he believes Boxer will roll out a lot of stores because it’s a very good model and it’s also low-cost. “Everyone is chasing space, so it’ll be tough, but it will be very hard to grow beyond the Shoprite group’s numbers because its stores are being rolled out aggressively.”

Distribution efficiency will be crucial for Boxer to compete effectively with Shoprite, which has a strong distribution network.

Independent retailers are also key competitors in this market. While they face intense competition and operate on low margins, they often offer alternative brands and discounted products, attracting price-sensitive consumers.

The battle for the lower-end retail market is only getting started, as Boxer, Usave, Shoprite and independent retailers are all poised for growth in this segment.

Ultimately, consumers will benefit from increased competition and a wider range of options, leading to potentially lower prices and improved product availability. DM

This article is more than a year old

Business Maverick

PnP’s Boxer needs ring smarts to beat Shoprite, Usave and a host of independent operators

South Africa’s retail landscape is undergoing a significant transformation as consumers grapple with the ongoing cost-of-living crisis. Times might be tough but for retailers, the lower end of the market is increasingly enticing because of large volumes, which is why Boxer’s imminent listing on the JSE will be keenly watched by the Shoprite Group.